Digital finance has become one of the most important forces shaping modern economies. It affects how people pay bills, transfer money, invest savings, borrow funds, shop online, and manage financial decisions every day. What once required a physical bank visit can now happen in seconds through a mobile device.

The rise of digital finance is not only about convenience. It also changes financial access, security systems, business models, and global economic behavior. In 2026, digital finance continues to expand rapidly through real-time payments, AI-driven banking tools, digital wallets, and cross-border payment innovations. In India especially, digital payment systems continue growing under stronger security rules from the Reserve Bank of India, including stricter authentication requirements introduced in 2026.

This article explains what digital finance means, how it works, why it matters, and what trends are shaping its future.

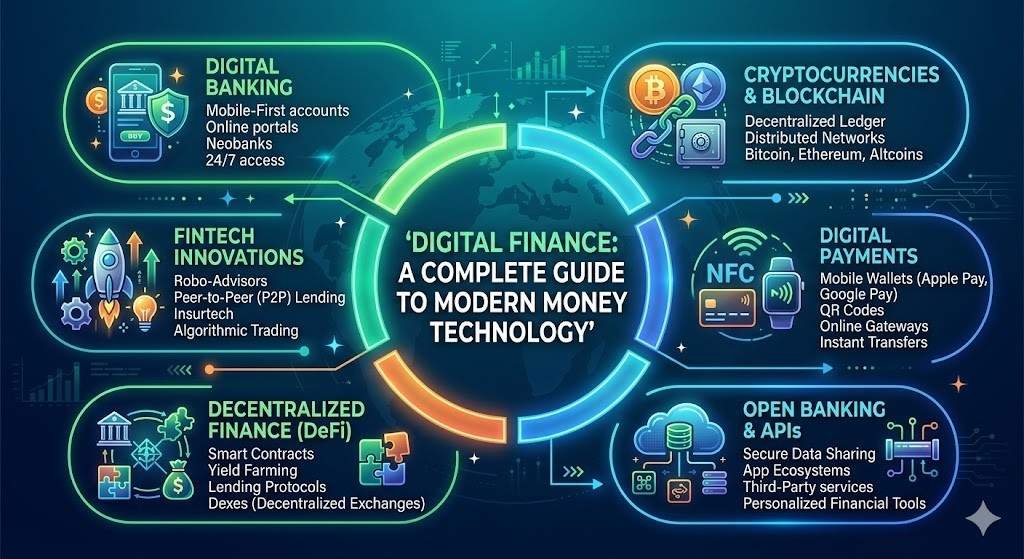

What Is Digital Finance?

Digital finance means using digital systems to access financial services instead of relying only on traditional physical banking.

It includes:

- Online banking

- Mobile payments

- Digital lending

- Investment apps

- Digital wallets

- Automated insurance systems

- Online money transfers

A person checking account balance through an app, paying electricity bills online, or receiving salary through digital transfer is already using digital finance.

Why Digital Finance Is Growing So Fast

Several global changes are driving this growth:

Mobile phone expansion

Smartphones have become the main financial tool for millions of users.

Faster internet access

Digital transactions now happen instantly.

Demand for convenience

People prefer quick financial actions without paperwork.

Business digitization

Companies increasingly operate online.

According to recent payment industry forecasts, digital wallets and instant payment systems are becoming dominant global payment tools.

Digital Payments Have Changed Everyday Spending

Digital payments are now central to daily life.

Popular payment forms include:

- QR code payments

- Mobile wallets

- Instant transfers

- Contactless cards

- Online checkout systems

In India, National Payments Corporation of India systems such as Unified Payments Interface have made digital payments part of daily routine.

Why people prefer digital payments

- Fast transactions

- Easy tracking

- Reduced cash handling

- Wide merchant acceptance

Digital Wallets Are Becoming Financial Hubs

Digital wallet is no longer only a payment tool.

Modern digital wallets may store:

- Payment cards

- IDs

- Loyalty points

- Utility payment history

- Transit access

Examples include:

- Google Pay

- PhonePe

- Paytm

Industry forecasts suggest wallets may become the main payment interface by 2030.

Online Banking Has Changed Traditional Banking Habits

Online banking allows customers to manage money anytime.

Common online banking actions:

- Fund transfer

- Balance checking

- Loan payments

- Fixed deposit management

- Statement downloads

Why online banking matters

It reduces physical branch dependence.

Banks now compete heavily on digital experience quality.

AI Is Becoming Central in Digital Finance

Artificial intelligence now supports many financial systems.

AI helps with:

- Fraud detection

- Spending alerts

- Credit scoring

- Personalized offers

- Customer support

More than fraud prevention, AI increasingly improves customer personalization in banking.

Example

A finance app may alert users before bills rise unusually.

Digital Lending Is Expanding Access to Credit

Digital lending makes borrowing faster.

Digital lending platforms offer:

- Personal loans

- Business loans

- Buy-now-pay-later options

Benefits

- Fast approval

- Less paperwork

- Wider access

Risks

- Over-borrowing

- Hidden fees

Investment Has Become More Accessible Through Apps

Digital finance has opened investing to beginners.

Popular digital investment tools allow:

- Mutual funds

- Stocks

- Gold investing

- SIP automation

Investors can now start with small amounts.

Security Is a Major Digital Finance Priority

As finance becomes digital, security becomes essential.

Security methods include:

- Biometric login

- Two-factor authentication

- Device verification

- Transaction alerts

India’s recent payment security rules show that OTP alone is no longer considered sufficient for some digital transactions.

Why this matters

Financial trust depends on strong security.

Cross-Border Digital Payments Are Becoming Faster

International transfers are improving rapidly.

New systems focus on:

- Faster settlement

- Lower fees

- Currency conversion efficiency

Recent fintech growth shows stablecoin-based payment infrastructure expanding for international transfers.

Embedded Finance Is Quietly Expanding

Embedded finance means financial tools inside non-bank apps.

Examples:

- Shopping app credit offers

- Ride app wallets

- Instant checkout financing

This trend allows finance to happen invisibly during normal digital activities.

Digital Finance Improves Financial Inclusion

One major benefit is broader access.

Digital systems help:

- Rural users

- Small businesses

- First-time bank users

People without traditional banking access may still join financial systems through mobile tools.

Challenges Facing Digital Finance

Despite growth, important challenges remain.

Cyber fraud

Fraud methods continue evolving.

Digital literacy gaps

Not all users understand safe practices.

Privacy concerns

Large financial data requires protection.

Regulation complexity

Rules must evolve with technology.

Digital Finance and Future Money Systems

Future developments may include:

- Central bank digital currencies

- Stablecoin expansion

- Smart contract payments

Research on digital payment design suggests central banks are actively studying secure digital currency models.

How Individuals Can Use Digital Finance Wisely

Good habits include:

- Use strong passwords

- Verify payment links

- Monitor statements regularly

- Avoid unknown apps

- Update devices often

Digital finance gives power, but safe use matters.

Why Businesses Depend on Digital Finance

Businesses use digital finance for:

- Payroll

- Billing

- Supplier payments

- Subscription models

Fast payment systems improve business cash flow.

Digital Finance by 2030

By 2030, likely trends include:

- Invisible payments

- AI financial assistants

- Real-time global transfers

- Stronger digital identity systems

Digital finance is moving toward systems that feel automatic but remain highly regulated.

Final Thoughts

Digital finance is changing how money moves, how people plan spending, and how businesses operate.

Its strongest advantages are:

- Speed

- Accessibility

- Flexibility

- Inclusion

Its biggest requirement is trust.

The future of finance will likely belong to systems that combine convenience with strong security and transparent regulation

FAQs –

1. What is digital finance?

Digital finance refers to financial services delivered through digital technology, including online banking, mobile payments, digital wallets, and investment apps.

2. How does digital finance work?

Digital finance works through internet-based platforms that allow users to transfer money, pay bills, save, invest, and manage accounts electronically.

3. What are examples of digital finance?

Examples include mobile banking apps, digital wallets, online payment systems, digital lending platforms, and investment applications.

4. Is digital finance safe to use?

Yes, digital finance can be safe when users follow security practices such as strong passwords, two-factor authentication, and trusted apps.

5. What is the difference between fintech and digital finance?

Fintech refers to financial technology companies and innovations, while digital finance is the broader use of digital systems for financial services.

6. How does digital finance help businesses?

It improves payment speed, reduces paperwork, supports online transactions, and helps businesses manage money more efficiently.

7. Can digital finance improve financial inclusion?

Yes, digital finance helps more people access banking and payment services, especially in areas with limited physical banking infrastructure.

8. What role does AI play in digital finance?

AI helps with fraud detection, customer support, spending analysis, and personalized financial recommendations.

9. Why are digital wallets becoming popular?

Digital wallets offer quick payments, convenience, secure storage of payment details, and easy access through smartphones.

10. What is the future of digital finance?

The future includes smarter payments, AI-driven banking, faster global transfers, stronger digital security, and wider financial access.

Also read :